How White Label Loyalty Software is Transforming Banks and Financial Institutions in 2026

- Editorial & Research Team

- |

- Published on January 28, 2026

On this page

Share Article

- By 2034, White Label Software market is projected to skyrocket to USD 61.47 billion.

- White label loyalty lets banks launch secure, branded programs in 8–12 weeks.

- AI-powered loyalty enables predictive, behavior-driven engagement beyond points.

- First-party data helps banks reduce churn and personalize at scale.

In 2026, the battle for the “top-of-wallet” position is no longer won by interest rates alone; it is won by relevance. As digital-first competitors erode traditional loyalty, 24% of financial institutions have pivoted to integrated platforms to combat rising churn.

White label loyalty software is a pre-built, API-driven rewards engine that banks can brand and embed directly into their existing digital infrastructure. By 2034, this market is projected to skyrocket to USD 61.47 billion, driven by a shift from transactional points to AI-powered emotional engagement.

For modern banks, the challenge isn’t just rewarding spend—it’s owning the data and the entire customer experience. By adopting a white label bank loyalty solution, banks can quickly roll out personalized, scalable loyalty ecosystems without heavy IT dependencies. In this guide, we explore how white label solutions are helping banks launch smarter loyalty programs in weeks, not years.

Understanding White Label Loyalty Software for Banks

White label loyalty software is a ready-built loyalty platform that banks can brand as their own. Instead of building loyalty tech from scratch, costly, time-consuming, and risky, institutions license customizable software that can be integrated directly into their apps, online banking portals, or digital wallets.

This enables banks to maintain complete control over their branding, customer data, and customer support while using innovative engagement tools such as reward programs, points, levels, games, and custom-tailored services that are integrated into the bank’s website and application interface (UX).

Why Financial Institutions Are Turning to White Label Loyalty

Banks face intense competition; digital banks are rising fast, fintechs are eating into market share, and consumer expectations for personalized experiences continue to climb. Here’s how white label loyalty platform directly addresses these challenges.

1. Increase Customer Retention & Engagement

Customer acquisition is costly, retention is profitable. Modern loyalty systems help banks:

- Reward actions like savings goals reached, credit card spend, referrals, or even daily app logins.

- Drive deeper engagement through personalized rewards and tailored journeys.

- Increase usage of digital banking products, reducing churn and boosting lifetime value (LTV).

Business Impact: Studies show a loyalty platform for banks makes customers significantly more likely to stick with a brand, a major win where wallets are competitive.

2. Differentiation in a Saturated Market

Financial services products can look similar, white label loyalty lets banks stand out by offering customized reward experiences that reinforce emotional connection and brand preference. This goes far beyond generic points programs.

3. First-Party Data Collection and Insights

Loyalty engines collect real-time data on customer behavior, purchase patterns, channel preferences, and reward redemptions, enabling banks to build hyper-personalized offers and predictive models for churn, LTV, and feature adoption.

4. Lower Cost & Faster Time-to-Market

White label loyalty platforms are pre-built, saving the time and expense of custom development. Institutions can launch programs in a matter of weeks rather than months, perfect for agile market moves.

Enterprise-Grade Security: Building Loyalty on a Foundation of Trust

For financial institutions, a loyalty program is only as strong as its security framework. Implementing a white label solution doesn’t mean compromising on institutional standards. Modern platforms are built to “plug and play” without creating new vulnerabilities.

- Bank-Level Compliance: Ensure your partner provides SOC2 Type II certification, which validates not just the design, but the operational effectiveness of security controls over time.

- Data Residency & Sovereignty: In 2026, global regulations like GDPR and local data residency laws are non-negotiable. Look for platforms that allow for local data hosting to ensure customer PII (Personally Identifiable Information) never crosses restricted borders.

- Seamless API Integration (PSD3 Ready): The best white label solution uses an API-first architecture. This allows the loyalty engine to communicate with your core banking system via secure, encrypted gateways, enabling real-time reward triggers without slowing down your primary app performance.

- Zero-Knowledge Architecture: Advanced providers now use “zero-knowledge” data handling, meaning they can process rewards and triggers based on encrypted signals without ever needing to see or store raw sensitive financial data.

Build vs. Buy: The 2026 Strategic Decision

For many financial institutions, the debate isn’t about whether to implement loyalty, but how to deploy it. While an in-house build offers total customization, the opportunity cost in 2026 is often too high.

| Feature | Custom In-House Build | White Label Platform |

| Time to Market | 12 – 18 Months | 8 – 12 Weeks |

| Upfront cost | $250k – $500k+ | Optimized & Scalable (Licensing/SaaS) |

| Maintenance | Dedicated Internal Team | Vendor-Managed Updates |

| Security | Manual Audits & SOC2 | Pre-certified (SOC2, GDPR) |

| AI Features | Requires Data Science Team | Built-in Predictive Engines |

| Risk Profile | High (Development Delays) | Low (Battle-tested Tech) |

Banks Winning with White Label Loyalty

Example Behavior Incentivized:

- Rewards for active salary account relationships and savings milestones

- Cashback or points for credit card usage

- Tiers based on relationship balance or product usage

- Personalized offers for financial habits tied to predictive analytics

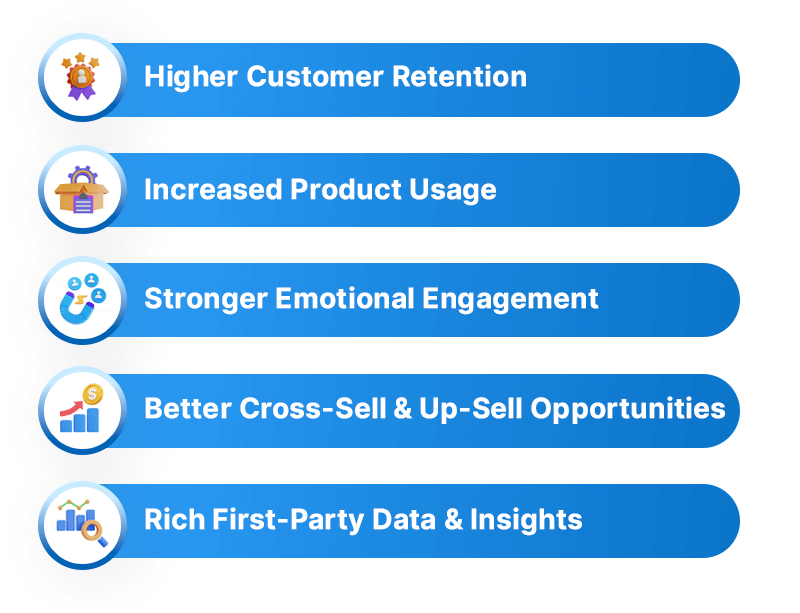

Key Loyalty Benefits for Banks

White Label Loyalty Drives:

Why 2026 Is a Loyalty Turning Point

With the increased options that customers have regarding who they bank with and how they interact with banking brands through digital means, banks can strategically leverage the loyalty of their customers, which is no longer just a nice-to-have but rather an important part of their overall strategies.

The introduction of white-label loyalty tools to financial institutions allows them to create a unique brand identity in the marketplace while also supporting their marketing strategies through instant access to customer engagement tools, detailed data analysis and research, and rapid implementation processes.

Financial institutions that invest in loyalty will always be better positioned to retain customers, increase the number of products used per customer, and prepare themselves for the future by providing predictive capabilities of their digital products and services as agile competitors continue to enter the market.

Final Thought

If your institution wants to retain more customers, increase engagement, and strengthen your brand’s bottom line, adopting a white label loyalty solution is no longer a “nice-to-have”; it’s a must-have growth engine. At Novus Loyalty, we help banks and financial institutions build powerful, customizable loyalty platforms that drive real outcomes, all under your brand. Discover how we can accelerate your loyalty strategy at novus-loyalty.com.

Explore Bank Loyalty

Build compliant, scalable loyalty programs for banking customers.